Author: Kelsey Matzinger

Financial Literacy

Published:

Monday, 24 Jun 2024

Sharing

.png/400w/50q)

Image caption: Since 2021, housing prices and interest rates have surged, creating a difficult environment for first-time buyers.

For over a century, owning a home has been synonymous with the American Dream. Since the 1890s, when homebuilders first linked homeownership with the promise of prosperity, generations of Americans have aspired to build wealth and create legacies through owning their own homes. However, recent trends reveal significant challenges facing young adults in achieving this milestone.

The Current Landscape: Challenges for Gen Z

Since 2021, housing prices and interest rates have surged, creating a difficult environment for first-time buyers. Real estate data firm Clever reports that housing prices are outpacing inflation by nearly two and a half times. Consumer Affairs highlights that this is part of a broader trend where essential costs have risen faster than wages, leading to Generation Z having 86% less purchasing power than Baby Boomers did at the same age.

Despite these challenges, Generation Z isn't entirely locked out of homeownership. Before the recent surges, Gen Z was on track to achieve higher homeownership rates than Millennials and Generation X at comparable stages in life. Even with rising prices, Gen Z is finding creative solutions, such as subleasing rooms and leveraging remote work opportunities in more affordable communities.

Barriers Beyond Affordability

Ideally, Generation Z shouldn't have to resort to unconventional living situations to afford homes. Beyond the rising prices and stagnant wages, many young adults face difficulties qualifying for mortgages due to high debt, low credit scores, and poor credit histories. These financial challenges often stem from large student loan debts and low pay, but poor financial management is also a factor. A lack of financial literacy, which isn't always taught in schools, plays a significant role.

Research by Junior Achievement reveals that while teens aspire to financial security, they often lack the necessary information to achieve it. This gap in financial education is a major hurdle for young adults hoping to navigate the complexities of homeownership.

The Price of the American Dream

These economic realities have significantly shaped how Gen Z views homeownership. Harvard University estimates that Gen Z will be the largest renter demographic by 2030, and one in three Gen Z-ers doesn't believe they will ever own a home.

Dispelling Myths: Gen Z's Desire for Homeownership

Contrary to popular belief, younger Americans are still interested in purchasing homes. A survey by Junior Achievement and Fannie Mae in 2022 found that most teens (88%) aspire to own a home someday, viewing it as part of "the good life." However, fewer than half (45%) of surveyed teens could correctly define a home mortgage, and 76% lacked a clear understanding of credit scores.

While nearly all teens (96%) believe credit scores are crucial for purchasing a home, around three-quarters (76%) admitted to only a partial understanding of them. The survey also revealed disparities in financial knowledge among different demographic groups, underscoring the need for better financial education.

An Optimistic Outlook

Despite these challenges, teens remain optimistic about homeownership. Even though more than a quarter (29%) have experienced housing instability due to foreclosure or inability to pay rent, they still hold favorable views on owning a home.

.png/400w/50q)

The Importance of Financial Literacy

At Junior Achievement, we emphasize financial literacy as "the other literacy." Just as with reading and writing, financial literacy is essential for daily life. Unfortunately, financial education often consists of a single semester elective in middle or high school, which is insufficient for mastering complex financial concepts.

How Junior Achievement Promotes Financial Literacy:

- Curriculum: Age-appropriate materials covering budgeting, saving, investing, and understanding credit.

- Hands-on Learning: Interactive exercises, simulations, and games that make financial concepts practical and engaging.

- Volunteer-Led Programs: Volunteers from the business community share real-life experiences, connecting classroom learning to the real world.

- Impact Measurement: Assessments and surveys to measure program effectiveness and refine the curriculum.

Positive Outcomes

Our approach equips students with the tools needed for economic security. Research by Ipsos shows:

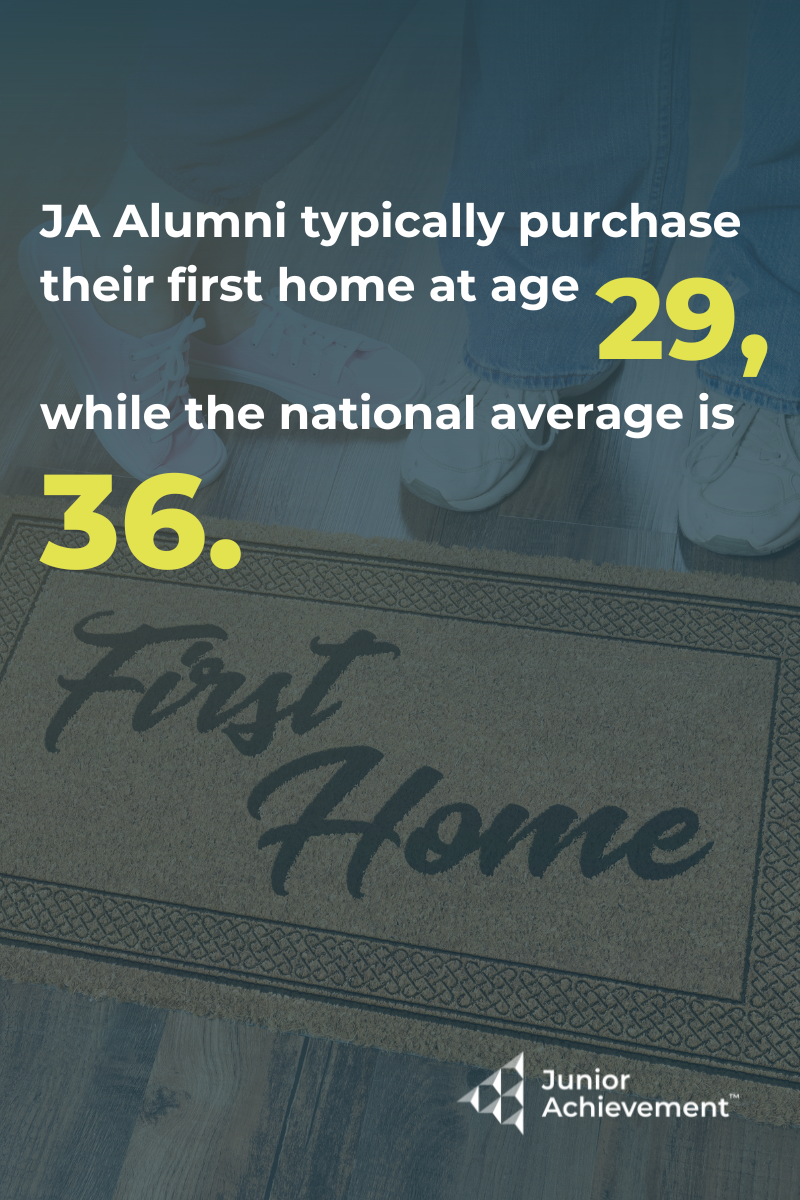

- JA Alumni typically purchase their first home at age 29, while the national average is 36.

- 82% of JA Alumni report a strong financial footing.

- 68% of JA Alumni aged 18-29 are financially independent of their parents, compared to 30% of Americans in the same age range.

While the path to homeownership for Generation Z is fraught with challenges, there is hope. Through improved financial literacy and innovative solutions, young adults can still achieve the American Dream of owning a home. At Junior Achievement, we are committed to empowering the next generation with the knowledge and skills necessary to turn this dream into reality.

Get Involved with Junior Achievement!

Select a button below to see how you or your organization can get involved with Junior Achievement of Acadiana.